Loans: Understanding Secured vs. Unsecured Loans

Loans are one of the most important financial tools for both individuals and businesses. They provide access to funds that can be used to achieve financial goals, cover emergencies, or make large purchases such as homes and vehicles. However, not all loans are the same. The two main categories secured loans and unsecured loans differ significantly in terms of risk, eligibility, interest rates, and borrower implications.

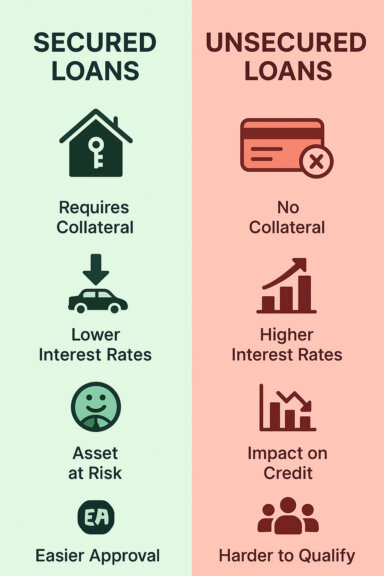

Understanding these differences is crucial when choosing the right financing option. Secured loans require collateral, while unsecured loans depend solely on the borrower’s creditworthiness. Each type comes with distinct advantages and disadvantages, making it important to align the choice with your financial situation and long-term goals.

What is a Secured Loan?

A secured loan is a type of borrowing that requires the borrower to pledge an asset, known as collateral, as security for the debt. If the borrower defaults, the lender has the legal right to seize and sell the collateral to recover the outstanding balance.

Common Examples of Secured Loans:

- Mortgages, where the property itself is the collateral.

- Auto loans, secured by the financed vehicle.

- Home equity loans or lines of credit, using property value as security.

Because the lender faces less financial risk, secured loans typically come with lower interest rates, higher borrowing limits, and longer repayment terms compared to unsecured loans. This makes them particularly suitable for major purchases such as real estate or cars, where large loan amounts and extended repayment periods are often necessary.

However, there are also risks. In the event of missed payments, the borrower could face foreclosure (in the case of a mortgage) or repossession (in the case of a car loan). This means that while secured loans may be more affordable in terms of interest rates, they carry the significant downside of potentially losing valuable property.

What is an Unsecured Loan?

An unsecured loan is a type of borrowing that does not require collateral. Instead of relying on a pledged asset, lenders base their decision on the borrower’s credit history, income, and overall financial stability. This makes unsecured loans more accessible for individuals who may not own valuable property but still need financing.

Common Examples of Unsecured Loans:

- Personal loans for expenses such as debt consolidation, home improvements, or medical bills.

- Credit cards, which provide revolving credit up to a pre-set limit.

- Student loans, designed to finance education, often with government support or special repayment options.

Since lenders face greater risk without collateral, unsecured loans generally come with higher interest rates and stricter eligibility requirements. Borrowers with strong credit scores and stable income are more likely to qualify for favorable terms, while those with lower credit may face higher costs or difficulty in approval.

For borrowers, one of the main advantages is that there is no risk of losing a physical asset like a home or car. However, failing to repay an unsecured loan can severely harm credit scores, limit future borrowing opportunities, and potentially result in collection actions or wage garnishment.

In short, unsecured loans offer flexibility and speed, but they also demand careful financial planning to avoid high costs and long-term credit damage.

Secured vs. Unsecured Loans: Key Differences

When deciding between a secured and an unsecured loan, it is important to evaluate how each option aligns with your financial needs, risk tolerance, and borrowing capacity. Both types serve different purposes, and understanding their distinctions can help you make the right choice.

Interest Rates

- Secured loans generally offer lower interest rates because collateral reduces the lender’s risk.

- Unsecured loans usually carry higher interest rates to compensate for the lack of collateral.

Loan Amounts

- Secured loans allow for larger borrowing limits, making them ideal for financing major purchases such as homes or vehicles.

- Unsecured loans typically provide smaller amounts, better suited for short-term expenses or emergencies.

Approval Process

- Secured loans often take longer to approve due to property valuation and additional paperwork.

- Unsecured loans are usually faster to obtain, as approval relies mainly on credit history and income.

Risks

- With a secured loan, the borrower risks losing the pledged asset (house, car, or property) in case of default.

- With an unsecured loan, there is no risk to physical assets, but default can damage credit scores and lead to legal or financial consequences.

Flexibility

- Unsecured loans offer more flexibility, as the funds can usually be used for any purpose without restrictions.

- Secured loans may be tied to specific uses, depending on the type of collateral involved.

| Aspect | Secured Loan | Unsecured Loan |

|---|---|---|

| Interest Rates | Lower | Higher |

| Loan Amounts | Higher | Lower |

| Approval Time | Longer | Faster |

| Risk | Loss of asset if default | Credit score damage, legal action |

| Flexibility | Limited use, depends on collateral | More flexible, multiple uses |

When to Choose a Secured Loan

Secured loans are the best option in situations where you need access to large amounts of money with lower interest rates and longer repayment terms. Because they are backed by collateral, they allow borrowers to obtain financing under more favorable conditions compared to unsecured loans.

Buying a Home

The most common example of a secured loan is a mortgage, where the property itself serves as collateral. This structure makes it possible for lenders to provide higher amounts and longer terms, making homeownership accessible. For more details, you can review the U.S. Department of Housing and Urban Development’s mortgage resources.

Financing a Vehicle

Car loans are another form of secured loan, where the vehicle is used as collateral. Interest rates are generally lower than personal loans, and repayment terms are aligned with the expected lifespan of the car.

Debt Consolidation

If you have multiple high-interest debts, using a home equity loan or line of credit as a secured option can help consolidate them into one payment with lower interest rates. This not only reduces financial stress but also simplifies debt management.

Key Consideration

While secured loans provide more affordable borrowing, the major risk lies in the possibility of losing your property if payments are not made on time. Careful planning and realistic budgeting are essential before committing.

When to Opt for an Unsecured Loan

Unsecured loans are a good choice when you need quick access to funds, do not want to risk assets as collateral, or only require smaller loan amounts. They are faster to obtain but come with higher interest rates and stricter approval requirements.

Covering Emergencies

Unsecured personal loans are often used to manage unexpected expenses such as medical bills or urgent home repairs. Because no collateral is needed, approval can be faster, allowing borrowers to access funds quickly. For tips on handling emergency expenses responsibly, visit the Consumer Financial Protection Bureau (CFPB).

Managing Smaller, Short-Term Expenses

Credit cards are one of the most common forms of unsecured credit. They provide ongoing access to funds with a pre-set limit, which can be useful for short-term or everyday purchases. However, interest rates can be very high if balances are not paid in full each month. Learn more about responsible credit card use at the Federal Trade Commission.

Financing Education

Student loans are another example of unsecured borrowing, specifically designed to cover education-related expenses. Some programs backed by the government may offer lower interest rates or flexible repayment plans. Detailed information on federal student aid can be found on the Federal Student Aid website.

Key Consideration

While unsecured loans protect your assets from repossession, they can have a lasting impact on your credit score if payments are missed. They also tend to be more expensive in the long run due to higher interest rates. Borrowers should ensure they can handle repayment comfortably within their monthly budget.

Conclusion

Choosing between a secured and an unsecured loan ultimately depends on your financial needs, credit profile, and tolerance for risk.

-

Secured loans are best suited for major investments like buying a home or car, or consolidating debt with lower interest rates and higher loan limits. However, they require collateral, and failing to meet payments could result in the loss of valuable assets.

-

Unsecured loans, on the other hand, provide flexibility and faster approval for smaller or emergency expenses, without putting property at risk. Yet, they come with higher interest rates, shorter repayment terms, and stricter eligibility requirements.

The right choice will depend on your financial stability, repayment capacity, and long-term goals. Always compare interest rates, terms, and conditions from multiple lenders before committing. Responsible borrowing can not only meet your immediate financial needs but also strengthen your overall credit health.

About the author

I have completed studies in law and marketing, and professionally I specialize in creating strategic content, branding, and social media management. I’m passionate about finance and communication, and my mission is to simplify complex topics and deliver valuable, accessible information. I’m communicative, organized, and I love fashion and good shopping. In my free time, I enjoy spending time in nature, cooking, traveling, and consuming content that sparks my curiosity and desire to learn.