Fixed Rate Bonds vs Easy Access Savings: Which Is Best for Your Money?

In the world of personal finance and investment, deciding where to place your money is rarely straightforward. Each choice carries implications for both security and growth. Two popular options are fixed rate bonds and easy access savings accounts, both of which serve different financial goals and risk appetites.

While fixed rate bonds provide certainty and predictable returns, easy access savings accounts offer flexibility and liquidity, allowing you to withdraw funds whenever needed.

In this guide, we will explore:

- What fixed rate bonds are and why they appeal to conservative savers.

- How easy access savings accounts work and when they are most suitable.

- A clear comparison of returns, risks, and accessibility.

- Practical tips for choosing the right option based on your financial objectives and time horizon.

By the end, you will have the knowledge to decide whether guaranteed stability or flexible access aligns better with your savings strategy.

Fixed Rate Bonds: What They Are and How They Work

Fixed rate bonds are a type of savings product where you deposit a lump sum for a set period, known as the term. In exchange, the provider pays you a guaranteed interest rate, which remains unchanged until the bond matures.

This predictability makes fixed rate bonds especially attractive to individuals who prefer stable returns and a clear income stream, regardless of market fluctuations.

Key Features of Fixed Rate Bonds

- Guaranteed interest – the rate is locked in from the start and does not change.

- Defined term – typically ranging from 1 to 5 years, though longer options exist.

- Regular interest payments – often annual or monthly, depending on the product.

- Security – usually offered by banks or building societies, with FSCS protection (up to £85,000 per person, per institution).

- Limited access – withdrawing before maturity may result in penalties or loss of interest.

Easy Access Savings Accounts: Flexibility and Convenience

Easy access savings accounts are designed for individuals who value flexibility and instant access to their money. Unlike fixed rate bonds, which lock your funds away for a set term, these accounts allow you to deposit and withdraw at any time without penalties.

They are particularly useful for short-term savings goals or as an emergency fund, where accessibility is more important than maximising returns.

Key Features of Easy Access Savings Accounts

- Instant access – withdraw funds whenever needed without restrictions.

- Variable interest rates – rates may rise or fall depending on market conditions.

- Low minimum deposits – usually accessible with small starting amounts.

- No fixed term – keep your money in the account as long as you like.

- FSCS protection – balances up to £85,000 per person, per institution are covered.

Advantages of Easy Access Savings Accounts

- Financial flexibility – ideal for covering unexpected expenses or short-term savings goals.

- Simplicity – easy to open and manage, often online or via mobile banking.

- Responsive to rate changes – if the Bank of England base rate rises, savings rates may improve.

Potential Drawbacks to Consider

- Lower interest rates compared to fixed rate bonds.

- Variable returns – rates can decrease at any time, reducing growth potential.

- Impact of inflation – if inflation is higher than your interest rate, the real value of your savings may fall.

Fixed Rate Bonds vs Easy Access Savings: Returns, Risks and Accessibility

Both fixed rate bonds and easy access savings accounts can play a role in a well-balanced savings plan. The best choice depends on your time horizon, need for access, and rate expectations. For broader context on how UK savings rates move with monetary policy, see the Bank of England Bank Rate. Guidance on savings products and consumer protections is available from the Financial Conduct Authority (FCA), and coverage limits for eligible deposits are outlined by the Financial Services Compensation Scheme (FSCS).

Returns

Fixed rate bonds pay a guaranteed rate for a set term, which can help you plan your income precisely. You lock in the rate at the outset and keep it for the entire term, regardless of market moves. By contrast, easy access savings accounts have variable rates that can rise or fall in response to market conditions and the provider’s pricing decisions. When the Bank Rate increases, easy access rates often improve (though not always by the same amount or at the same speed). Conversely, they can be reduced if market rates fall.

Risks

Credit and provider risk: For eligible UK banks and building societies, deposits are typically covered by the FSCS up to the applicable limit per person, per authorised institution. Always confirm your provider’s status and how the limit applies, especially if you hold multiple brands under the same licence.

Interest rate & reinvestment risk: With fixed rate bonds, you risk missing future, potentially higher rates while your money is locked. With easy access, rates can be cut, reducing future returns.

Inflation risk: If inflation outpaces your interest, the real (inflation-adjusted) value of savings can decline. Consider reviewing inflation data alongside your savings strategy; practical guidance on maintaining an emergency fund and choosing account types is available via MoneyHelper.

Accessibility

Easy access savings excel here: you can withdraw whenever you need without penalty, making them ideal for emergency funds and short-term goals. Fixed rate bonds usually restrict withdrawals until maturity; early access typically means penalties or loss of interest. If timing is uncertain, maintaining a liquidity buffer in easy access and using bonds for surplus funds can be a balanced approach (see MoneyHelper’s savings guidance).

| Feature | Fixed Rate Bonds | Easy Access Savings |

|---|---|---|

| Interest | Fixed for the full term | Variable; may change at any time |

| Access | Funds locked until maturity; penalties for early withdrawal are common | Withdraw at any time without penalty |

| Predictability | High (known returns) | Lower (rate can move up or down) |

| Best for | Medium to long-term savings where you won’t need the cash | Emergency funds and short-term goals |

| Protection | Eligible deposits typically covered by the FSCS (check provider and limits) | |

| Rate Drivers | Set at purchase; unaffected by later market moves | Often influenced by changes in the Bank Rate |

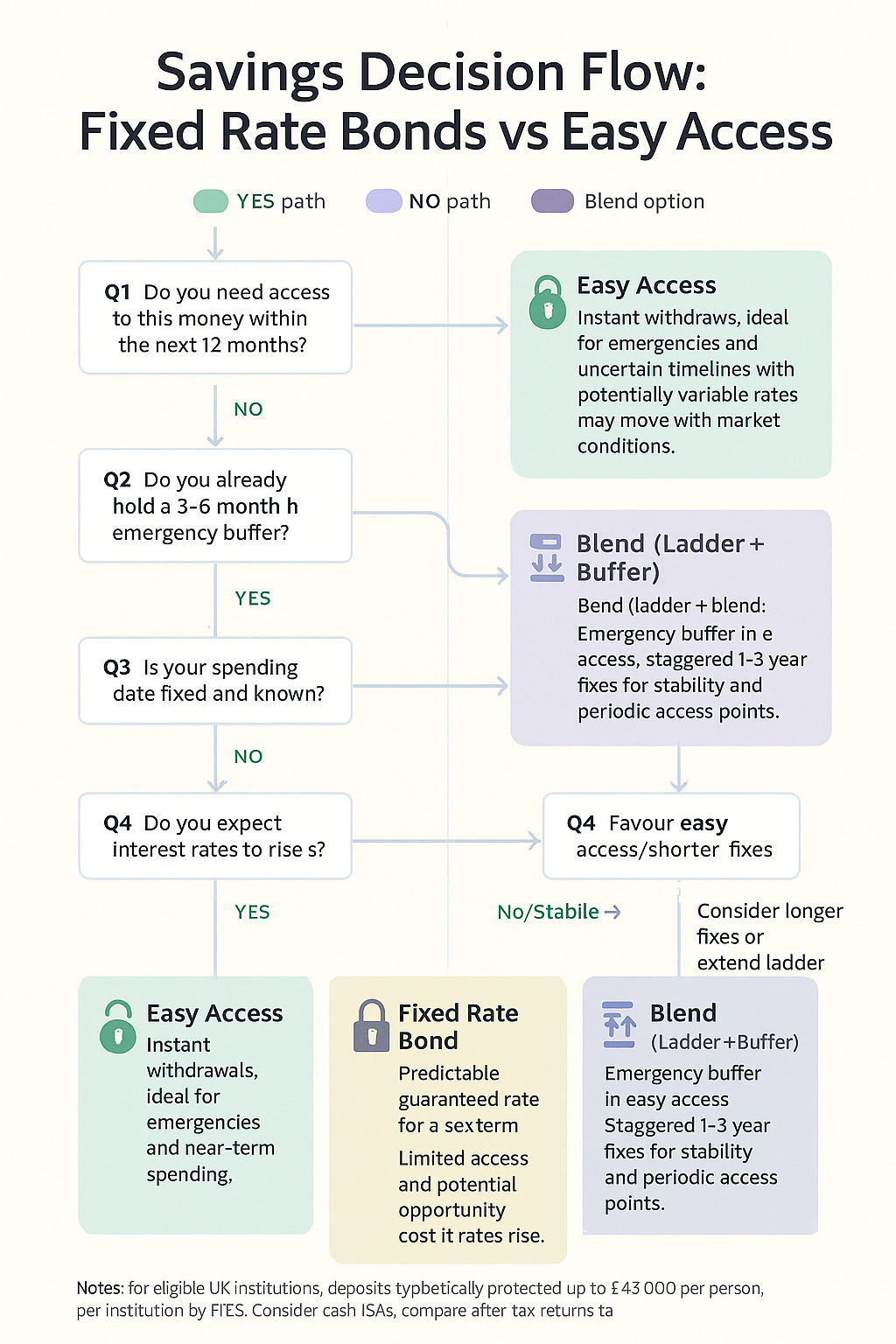

How to Choose Between Fixed Rate Bonds and Easy Access Savings

Choosing the right home for your cash depends on your goals, timing and comfort with changing interest rates. Use the checkpoints below to align the product with your priorities.

Match the Product to Your Timeframe

-

Short term (0–12 months): Easy access is usually more suitable, especially for upcoming expenses or uncertain timings.

-

Medium term (1–3 years): Consider a mix. A portion in fixed rate bonds for stability, with some cash kept liquid.

-

Long term (3+ years): Fixed rate bonds can lock in certainty, but keep a liquidity buffer for surprises.

Prioritise Liquidity Needs

- If you may need the money at short notice, favour easy access.

- If funds are ring-fenced for a specific future date, a fixed term can be appropriate.

Assess Your Risk Tolerance

-

Rate-change sensitivity: If falling rates would frustrate you, fixed can help.

-

Opportunity cost: If rising rates are likely and you want to benefit quickly, easy access adjusts faster.

Consider Tax Wrappers and Allowances

- Placing savings in appropriate tax-efficient accounts (e.g., cash ISAs in the UK) can improve net outcomes.

- If you already use tax wrappers elsewhere, weigh the after-tax return, not just the headline rate.

Plan for Inflation

- Compare expected inflation with your interest rate.

- Fixed rates provide nominal certainty; easy access rates can move, but not always fast enough to outpace inflation.

Practical Decision Tips

- Known date + no need for access = fixed rate bond is often sensible.

- Uncertain date or emergency fund = easy access first.

- Mixed goals = blend both (see strategy below).

Combining Both: Bond Ladder + Savings Buffer

Blending products balances stability with flexibility. Here’s a simple, repeatable framework.

Step 1: Build a Liquidity Buffer

- Aim for 3–6 months of essential expenses in an easy access account.

- Keep this ring-fenced as your emergency fund so you won’t need to break a bond early.

Step 2: Create a Bond Ladder

- Split the rest of your savings across staggered maturities (e.g., 1-year, 2-year, 3-year).

- As each rung matures, reinvest into a new longest rung to maintain the ladder.

- Benefits: regular access points, smoother reinvestment risk, and a steady rate profile.

Step 3: Automate Contributions and Reviews

- Automate monthly top-ups into easy access until your buffer target is met, then divert extras to the next ladder rung.

- Review every 6–12 months or after major life changes (new job, home move, dependants).

Worked Example (Illustrative)

- £12,000 emergency fund in easy access (covers ~4 months of essentials at £3,000/month).

- Remaining £24,000 laddered:

- £8,000 in a 1-year fix

- £8,000 in a 2-year fix

- £8,000 in a 3-year fix

- When the 1-year matures, roll it into a new 3-year. Repeat yearly to keep the ladder intact.

Common Pitfalls to Avoid

- Breaking a bond early due to insufficient buffer.

- Chasing headline rates without checking withdrawal rules or compounding frequency.

- All-or-nothing allocations that ignore real-life cash needs.

| Scenario | Best Fit | Why |

|---|---|---|

| Emergency fund (covering 3–6 months of expenses) | Easy Access Savings | Instant withdrawals, no penalties, ensures cash is ready when needed. |

| Saving for a house deposit (timeline uncertain) | Mainly Easy Access | Flexibility for withdrawals at short notice, without risking penalties. |

| Saving for a known expense (e.g. wedding in 2 years) | Fixed Rate Bond (2-year) | Locks in a guaranteed rate, aligns maturity with the spending date. |

| Medium-term growth (3–5 years) | Bond Ladder + Easy Access Buffer | Balances stable returns with rolling access points and liquidity cover. |

| Long-term savings (retirement top-up, 5+ years) | Fixed Rate Bonds (longer term) | Predictable returns over time, less need for immediate access. |

| Uncertain future rates (expecting changes) | Blend of Both | Protects part of savings with fixed rates while leaving some funds flexible. |

About the author

I have completed studies in law and marketing, and professionally I specialize in creating strategic content, branding, and social media management. I’m passionate about finance and communication, and my mission is to simplify complex topics and deliver valuable, accessible information. I’m communicative, organized, and I love fashion and good shopping. In my free time, I enjoy spending time in nature, cooking, traveling, and consuming content that sparks my curiosity and desire to learn.